Asia equities sharply higher, following US stocks

Asia market update: Asia equities sharply higher, following US stocks; Recapture levels pre-Black Monday and more (Aug 5th).

General trend

- Following last night’s US stock rally after better jobs data and higher US retail sales, shares opened up sharply higher in Japan and Korea (post-holiday), quickly followed by Australia and HK playing catch up. - Chipmakers SK Hynix +7% Tokyo Electron +5%, Renesas +6% with Advantest +4%. Technology in general was strong with Softbank +5% and major Nikkei component Fast Retailing +5%.

- The Nikkei +3.3% also enjoyed a weaker Yen again of 149, and having already recuperated its losses from Black Monday on Aug 5th is poised for a weekly gain of ~7.5%, which would be its best weekly performance since April 2020.

- In Australia the ASX 200 commodity sensitive indices were up; Energy +2.1%, Resources +2%; Financials +1.5% post Q3 results from NAB.

- The Hang Seng also rose by 1% at the open, following tech earnings out of JD.com and Alibaba overnight, along with PBOC support pledges from Gov Pan Gongsheng to implement already-introduced policies and measures and introduce additional measures.

- Japanese yields followed the overnight global trend higher, with JP 10-yr +4.5bps to on top of gains overnight to be 0.88% in early cash trading, with the Yen holding steady after falling back to 149 against USD overnight.

- After last week’s severe volatility in Japanese stocks, the week ended August 9th showed that foreigners bought a net half trillion Yen in Japanese stocks. While the 15% plunge of the Nikkei on Monday, Aug 5th no doubt saw significant selling of equities, by end of week the Nikkei had more or less recovered to its pre-Black Monday levels.

- China PBOC injected >1.1T Yuan of liquidity via open market operations during the week.

- In a continuation of the bond war between the China govt vs investors buying up bonds as a stable hedge of value, China’s regulator was reported to have provided “guidance” for mutual funds to restrict their fund allocations for 7-year China Treasury bonds.

- In trade news, Japan upped the ante concerning chips exports to China, adding chip equipment to products that are protected under the foreign trade law.

- Thailand Parliament voted in Paetongtarn Shinawatra as new Prime Minister; at just 37 Thailand's youngest ever PM and the nation's second female PM. Her popular father Thaksin was the first Thai politician ever to win an overall majority of seats.

- US equity FUTs +0.2% to +0.3% during Asian trading.

Looking ahead (Asian time zone)

- Fri Aug 16th (Fri night US Michigan Aug Consumer Sentiment).

Holidays in Asia this week

- Mon Aug 12th Japan, Thailand.

- Thu Aug 15th India, South Korea.

Headlines/economic data

Australia/New Zealand

- ASX 200 opens +0.3% at 7,887.

- Reserve Bank of Australia (RBA) Gov Bullock and staff: Board is of the view that it has the balance right between reducing inflation in a reasonable time frame while preserving jobs - Parliamentary testimony.

- Australia sells A$700M vs. A$700M indicated in 2.25% May 2028 bonds; Avg Yield: 3.5725% v 4.1383% prior; bid-to-cover: 3.83x v 4.08x prior.

- New Zealand July Manufacturing PMI: 44.0 v 41.2 prior (17th month of contraction).

- New Zealand Q2 PPI Input Q/Q: 1.4% v 0.7% prior; Output Q/Q: 1.1% v 0.9% prior.

- New Zealand July Non-Resident Bond Holdings: 59.6% v 60.7% prior.

- New Zealand Central Bank (RBNZ) Gov Orr: Follow up comments: Committee has achieved a very strong level of confidence that low and stable inflation is back within target 1-3% - financial press.

- New Zealand Central Bank (RBNZ) Asst Gov Silk: Measured approach on OCR cuts are appropriate (inline) - financial press interview.

China/Hong Kong

- Hang Seng opens +1.0% at 17,286; Shanghai Composite opens flat at 2,877.

- China Customs: To implement rules for movement of people and goods from areas with Monkeypox cases - Chinese press.

- China PBOC Gov Pan Gongsheng: China will gradually shift away from a focus on quantitative targets; China will improve the mechanism for forestalling and defusing systemic risks [overnight update].

- Alibaba Reports Q2 (CNY) 16.44 v 17.37 y/y, Rev 243.2B v 249.9Be; China commerce retail Rev -2% y/y; Notes cloud business achieved positive revenue growth momentum, driven by public cloud and AI-related product adoption [overnight update].

- China July Client FX Net Settlement (CNY): -327.5B v -282.2B prior [overnight update].

- China PBOC sets Yuan reference rate: 7.1464 v 7.1399 prior.

- China PBOC Open Market Operation (OMO): Sells CNY138B in 7-day reverse repos; Net injects CNY125B v net injects CNY571B prior.

Japan

- Nikkei 225 opens 1.6% at 37,304.

- Japan Jun Tertiary Industry Index M/M: -1.3% v +0.6% prior.

- Japan adds chip equipment to products that are protected under the foreign trade law – US financial press.

- Japan releases weekly flows data [period ended Aug 9th]: Foreign buying of Japan equities: +¥521.9B v -¥643.7B prior; Japan buying of foreign bonds: +¥1.54T v ¥677.7B prior.

- Japan sells ¥249.9B vs. ¥250B indicated in 10-year inflation-linked JGB Bonds; Yield at lowest accepted price: -0.4260% v -0.5450% prior, bid-to-cover: 2.96x v 4.27x prior.

- Japan FY25/25 (next fiscal year) budget request seen over ¥115T (record level) - Japanese press [overnight update].

South Korea

- Kospi opens 1.9% at 2,695 (recaptures levels prior to Mon, Aug 5th sell off).

- South Korea says impact from China's antimony export controls will be 'limited' - financial press.

Other Asia

- Thailand Parliament votes on new PM: Paetongtarn Shinawatra wins with 248 votes.

- Malaysia Central Bank (BNM) Gov Ghaffour: Headline and Core inflation seen remaining in forecast ranges of 2.0-3.5% and 2.0-3.0%.

- Philippine Central Bank (BSP) Gov Remolona: 2025 is the relevant policy horizon; reiterates might cut interest rates again sometime in 2024.

- (TW) Follow up: A second earthquake shakes buildings in Taipei, Taiwan; USGS Magnitude 6.1, centered off Eastern Coast, 26km SE of Hualien City - press.

- Singapore July Non-oil Domestic Exports M/M: 12.2% v 2.1%e; Y/Y: 15.7% v 1.2%e.

- Thailand Dep PM Phumtham to act as interim Prime Minster - financial press [overnight update].

- PHILIPPINES CENTRAL BANK (BSP) CUTS OVERNIGHT BORROWING BY 25BPS TO 6.25%; AS EXPECTED [overnight update].

North America

- (US) Republican VP candidate J.D. Vance confirms to debate Democrat VP Candidate Tim Walz on Oct 1st on CBS in NY City - US press.

- (US) Jun total net TIC flows: $107.5B V $15.8B prior; net long-term tic flows: $96.1b v -$54.6b prior.

- (US) Initial jobless claims: 227K V 235KE (lowest since early July); continuing claims: 1.864M V 1.87me.

- (US) Aug Philadelphia Fed business outlook: -7.0 V +5.2E (below all estimates); employment: -5.7 v +15.2 prior.

- (US) Aug empire Manufacturing index: -4.7 V -6.0E.

- (US) July advance Retail Sales M/M: 1.0% V 0.4%E; Retail Sales (ex-auto) M/M: 0.4% V 0.1%E.

- (US) July import price index M/M: 0.1% V -0.1%E; Y/Y: 1.6% V 1.5%E.

- (US) Weekly EIA Natural Gas inventories: -6 BCF VS. +5 BCF to +7 BCF indicated range (first negative reading since early April).

Europe

- REVOLUT.IPO (UK) UK Treasury Official reportedly to meet Revolut on IPO talks in Autumn - FT.

- (NO) Norway Central Bank (Norges) left the Deposit Rates unchanged at 4.50% (as expected).

Levels as of 01:20 ET

- Nikkei 225 +3.2%; ASX 200 +1.0%; Hang Seng +2.0%; Shanghai Composite +0.1%; Kospi +2.3%.

- Equity S&P500 FUTs +0.2%; Nasdaq100 FUTs +0.3%, Dax +0.1%; FTSE100 -0.1%.

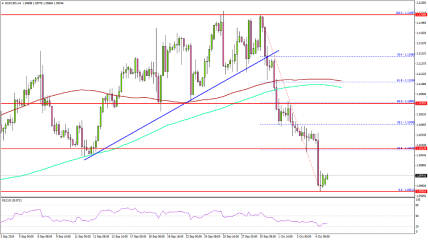

- EUR 1.10971-1.0984: JPY 148.74-149.35; AUD 0.6607-0.6633; NZD 0.5978-0.6026.

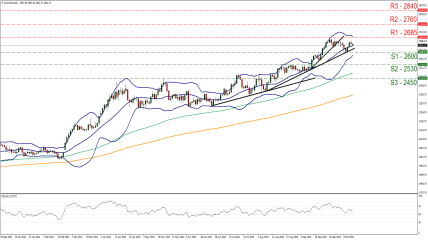

- Gold -0.1% at $2,490/oz; Crude Oil -0.5% at $77.88/brl; Copper -0.2% at $4.1355/lb.

Recommend Broker

https://one.exnesstrack.net/boarding/sign-up/a/uq2cbl5o/?campaign=24533