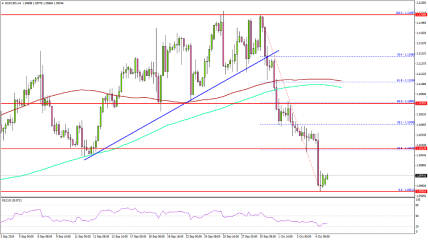

EUR/USD Weekly Forecast: Tension mounts ahead of US inflation, ECB announcement

The EUR/USD pair changed course after extending its slide to 1.1025, finding some positive footing mid-week to settle near 1.1100 after peaking at 1.1154 on Friday.

The focus remained on macroeconomic data that could affect the upcoming central banks’ monetary policy decisions. In the Eurozone, news gyrated around growth-related figures, while in the US, investors kept an eye on updates about the labor market.

Tepid European progress ahead of the ECB

Slow EU economic progress kept limiting the Euro’s strength. The manufacturing sector saw modest progress in August, as the Hamburg Commercial Bank (HBOC) upwardly revised the Manufacturing Purchasing Managers Index (PMI) for the region but resulted at 45.8, still indicating economic contraction. The Services PMI, on the other hand, was downwardly revised to 52.9, resulting in a Composite PMI of 51.0.

With ECB officials repeating that decisions are data-dependent, the movement has been priced in long ago. On the one hand, inflation keeps closing into the central bank’s 2% goal. On the other hand, because of tepid economic progress due to the restrictive policy, the rate cut was already priced in long ago, and what can actually affect the Euro is whatever forward guidance policymakers are willing to offer.

Beyond the ECB announcement, the EU will have little to offer. The Union will release September Sentix Investor Confidence on Monday and July Industrial Production on Friday, while Germany will publish the final estimate of the August Harmonized Index of Consumer Prices (HICP) on Tuesday.

United States employment data ahead of Fed

Speculative interest welcomed tepid United States (US) employment-related figures that fueled speculation the Federal Reserve (Fed) could deliver a 50 bps rate cut when it meets in mid-September.

The country released the ADP report on Employment Change, which showed that the private sector added 99,000 new job positions in August, well below the 145,000 anticipated. At the same time, the Challenger Job Cuts report showed that layoffs in August soared to 75,891, while year-to-date hiring reached a historic low.

More employment-related data showed that Initial Jobless Claims in the week ended August 30 hit 227K, below the 230K expected and the previous 232K. The number of job openings on the last business day of July stood at 7.67 million, according to the JOLTS Job Openings report released by the US Bureau of Labor Statistics (BLS). The reading was well below the 8.1 million expected.

Meanwhile, the country published the August ISM Manufacturing Purchasing Managers Index (PMI), which improved to 47.2, below the 47.5 expected. The Services PMI for the same month grew by more than anticipated, as the index hit 51.5 vs. the 51.4 posted in July and the 51.1 expected.

Finally on Friday, the US published the Nonfarm Payrolls (NFP) report, which showed that the US economy created 142,000 new jobs in August, less than the 160,000 expected. Even further, the July headline reading was downwardly revised to 89,000. The Unemployment Rate ticked down to 4.2%, as expected, while the Labor Force Participation Rate held steady at 62.7%.

The USD seesawed between gains and losses with the NFP report, as the figures were weak enough to back a Fed rate cut but not as weak as to trigger recession-related concerns. A 25-basis-point trim is the most likely scenario as US policymakers enter a blackout period ahead of the monetary policy announcement, scheduled for September 18.

The central bank is also expected to continue to allow up to $25 billion in Treasury securities and $35 billion in agency mortgage-backed securities (MBS) to mature and roll off its balance sheet per month. The balance sheet has dropped from a record high of $8.9 trillion in May 2022 to around $7.1 trillion in September, although it is still above pre-pandemic levels. Finally, the Fed will update its economic projections with a fresh view of where growth, inflation, and employment are expected to be in the next couple of years.

The US will publish the August Consumer Price Index (CPI) next Wednesday, while the Producer Price Index (PPI) for the same month will be out the following day. At the end of the week, the country will publish the preliminary estimate of the September Michigan Consumer Sentiment Index.

REGISTRATION LINK 👇🏻

https://one.exnesstrack.net/a/xfbfc8hw70