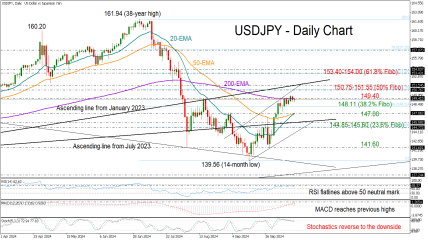

Markets poised for Nvidia earnings

In focus today

In Sweden, today's foreign trade data for July will give some preliminary insight into Q3 activity. Riksbank vice governor Anna Breman gives a speech on climate and monetary policy at 13:00 CET.

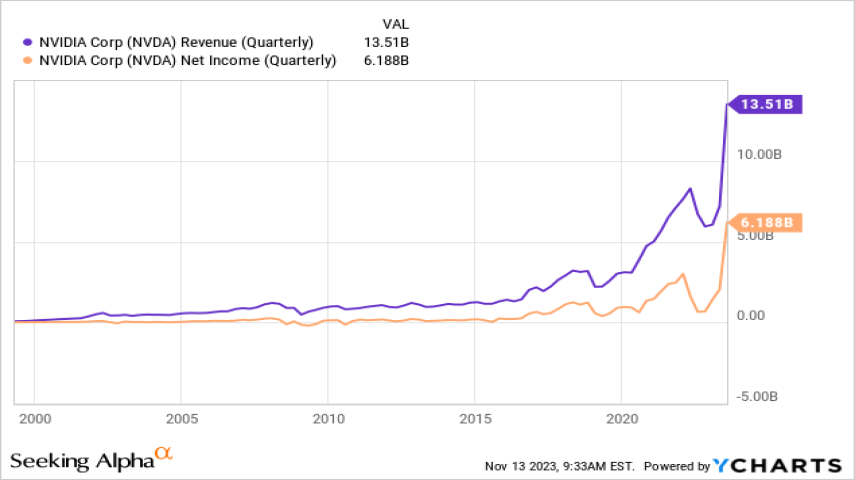

NVIDIA quarterly earnings are due tonight. The company, which moves up and down in the top 3 most valuable listed US stocks, has become the face of the AI tech boom and markets have used its earnings calls to assess the status of AI capex spending. Thus, it has the potential to move global markets despite being scheduled after US market close.

Economic and market news

What happened overnight

Australian inflation came in a bit higher than expected at 3.5% in July (cons.: 3.4%), which prompted Asian shares to slip and sent Australian yields slightly up as markets lowered the odds of a November cut from the RBA.

What happened yesterday

In the US, the Conference Board consumer survey improved more than expected with the overall index at 103.3 (cons.: 100.7). The details revealed that consumers see lower odds of a recession, expect substantially lower inflation (4.9% from 5.3%), and a weaker labour market; all in line with the prevailing market narrative post-Jackson Hole, which currently sees a 25bp cut fully priced in for the September meeting. As such the market impact was muted.

Oil nearly reversed Monday's gains with Brent at 79.66 USD/bbl. as of this morning. The move seems to be driven in part by expectations of lower growth following the Fed's dovish comments, and in part by reports that the risk of further escalation between Israel and Hezbollah seems to have diminished.

In geopolitics, Ukrainian President Zelenskiy is ready to present a peace plan to the US government and potentially the presidential candidates in September, with recent Ukrainian incursions into Russian territory being part of this plan.

ECB Governing Council member Knot was slightly hawkish stating a September cut was not a done deal, contrary to what markets are pricing, citing lack of data.

Equities: Global equities were marginally higher yesterday, showcasing a very mixed sector and regional performance. However, large-cap cyclicals continued to outperform, with US tech performing well and implied volatility slightly decreasing. As we approach the end of the week, we anticipate more intriguing micro and macro news that will likely spur greater activity, especially in the equity markets. In the US yesterday, Dow +0.02%, S&P 500 +0.2%, Nasdaq +0.2%, and Russell 2000 -0.7%. Asian markets are lower this morning, and the same trend is observed in most US markets. European futures are higher again today, despite the headwinds from a stronger euro.

FI: Long-end EGB yields edged higher throughout yesterday's session, with the 10Y Bund yield settling just shy of the 2.30% threshold. In contrast, short-end yields remained relatively stable, as markets continue to anticipate approximately 65bp in ECB rate cuts by year-end. The 5y5y EUR inflation swap rate climbed by about 4bp to 2.575%, reflecting recent increases in commodity prices. Concurrently, the Bund ASW spread has tightened, now trading at 28.7bp, amid diminishing risk premiums and sustained high activity in the primary market.

FX: After the big moves last week this week has failed to bring any bigger moves in G10 FX. The CHF and the NOK were an unusual set of outperformers yesterday, but the gains were still limited to less than 1 standard deviation from a historical perspective.

REGISTRATION LINK 👇🏻

https://one.exnesstrack.net/boarding/sign-up/a/uq2cbl5o/?campaign=24533