The Dollar and rates come back firmer

Overview: The US dollar's decline continued yesterday after the steep jobs’ revision and an unusual solid auction of the Treasury's 20-year bond. The minutes from the recent meeting confirmed that the FOMC will begin its easing cycle next month. The dollar is mostly firmer today. The market has looked through the stronger than expected eurozone flash PMI--seeing the impact of the Olympics--and stalled the euro's rally, which lifted it to new highs for the year yesterday. The UK's flash PMI was also stronger than expected but sterling has been rewarded and extend its advance to near last year's high (~$1.3140). A rail strike in Canada has not prevented an extension of the Canadian dollar's recovery, and it is trading at its best level in four months. The greenback is firmer against nearly all the emerging market currencies today save the Philippine peso, Malaysian ringgit, and the Russian ruble.

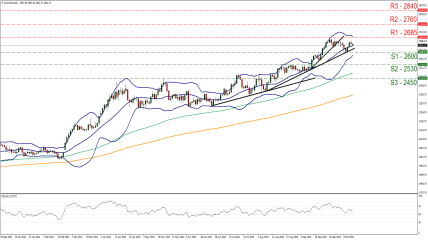

Equities are mostly higher. In the Asia Pacific region, China and Taiwan are notable exceptions. The MSCI Asia Pacific Index rose 4.25% last week and is up almost 1% this week. The Stoxx 600 in Europe is up about 0.65% today. It is up about 1.1% this week after a nearly 2.5% gain last week. US index futures are flattish. The S&P 500 is up 1.2% this week coming into today after a nearly 4% gain last week. The Nasdaq is up 1.6% so far this week after a 5.3% rally last week. European 10-year bond yields are up 2-3 bp today. The 10-year US Treasury yield is slightly firmer near 3.82%, after falling for the past four sessions. The two-year Treasury yield is up a little more than two basis points to 3.95%. It has fallen 13 bp in the past two sessions. The firmer dollar and rates are facilitating a consolidative tone for gold, which is trading inside yesterday’s range, hovering around $2500. October WTI is little changed, stuck in a narrow range (~$71.60-$72.10) in the lower end of yesterday's range (~$71.45-$74.15).

Asia Pacific

Japan's preliminary August PMI showed little improvement. In July, the manufacturing PMI slipped back below 50 and remained there in August (49.5 vs. 49.1). In May and June, it had risen above the boom/bust level for the first time since October 2022. May's 2023 one-month wonder when it rose above 50 was a bit of a statistical fluke. Growth of the service sector (54.0 vs. 53.7 in July) kept the composite firm at 53.0, ta marginal new high since May 2023). Separately, Japan reported its weekly portfolio flows. Japanese investors continued to buy foreign bonds and stocks. They have bought more foreign assets over the past six weeks than any other six-week period this year (~JPY3.8 trillion or ~$26 bln). The yen's appreciation is not a function these investors repatriating funds but rather they are taking advantage of the yen's appreciation to buy more foreign assets. Foreign investors sold a small amount of Japanese stocks last week but continued to plough money into the Japanese bond market. Over the last six weeks, foreign investors bought JPY3.4 trillion Japanese bonds. First thing tomorrow, Japan reports July CPI. The Tokyo rep ort a few weeks ago signals a small decline in the headline rate and a small rise in the core rate, which excludes fresh food. Australia's preliminary August manufacturing PMI rose to 48.7 from 47.5. Outside of January 2024, when it reached 50.1, the last time it was above 50 was in February 2023. Growth in the service sector accelerated and the PMI rose to 52.2 from 50.4. The composite rose for the first time in five months and moved back above 50 (51.4 from 49.9).

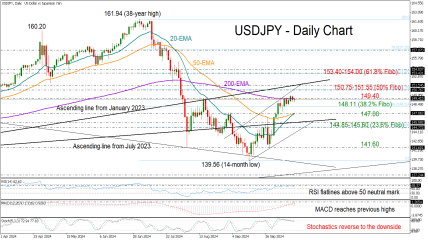

Pulled lower by its broad weakness and the decline in US 10-year yield, which fell below 3.80% for the first time in two weeks, the greenback made new session lows near JPY144.50 in the North American afternoon yesterday. It is trading quietly today inside yesterday's range and confined so far to roughly JPY144.85-JPY145.65. Through the first three sessions this week the dollar has recorded lower highs and lower lows. Unlike earlier bouts of yen strength, other G10 currencies did not sell-off and the S&P and NASDAQ traded higher. Still, some reports continue to stress the unwinding of residual carry trades and cite the weakness of Latam currencies, and especially the Mexican peso. Today, the yen and the peso are softer. The surge of the yen in the second half of July and into early August, saw the Australian dollar plummet from $0.6800 to $0.6350. However, the Aussie remained firm, traded in a narrow range in North America, mostly about 15-ticks on either side of $0.6745. The midpoint of today's narrow range is slightly lower (~$0.6740), and it will snap the four-day setting of higher highs and higher lows. The greenback traded at two-and-a-half week lows against the offshore yuan yesterday, but the low was set in the local session and the push to new dollar lows against the yen did not translate to a new low against the offshore yuan. Still, the US dollar settled below CNH7.12. Tracking its performance against the yen today, the greenback is trading firmer against the offshore yuan. It has recovered to about CNH7.14. The PBOC set the dollar's reference rate at CNY7.1228 (CNY7.1307 on Wednesday and CNY7.1464 last Thursday). Three-month implied CNH vol rose a slightly above 6.15% yesterday, its highest level since last August but settled ever so slightly below 6.0%. It is a little lower today. In the current environment, a stronger yuan is consistent with higher implied volatility.

Europe

The euro's rally to its best level since the end of last year is not a reflection of strong economic performance. And this is the message from the flash August PMI. The aggregate manufacturing reading remains below 50 (45.6 from 45.8), while the service PMI jumped to 53.3(from 51.9). But the gain in service PMI appeared linked to the Paris Olympics, which flattered the EMU composite PMI (51.2 from 50.2). Germany's manufacturing and service PMI softened, and the composite fell to 48.5 from 49.1. France's manufacturing PMI fell to 42.1 from 44.0. The service PMI surged to 55.0 from 50.1, and the composite rose to 52.7 from 49.1. The UK was the strongest economy in the G7 in H1, and although it is expected to moderate in H2, the August PMI suggests activity remains firm. The manufacturing and service PMI readings improved, and the composite rose to 53.4 from 52.8, a four-month high. The UK's composite PMI has not been below 50 since last October.

The euro and sterling set new highs for the year yesterday. The euro reached nearly $1.1175. It has not been that high since July 2023, when it peaked a cent higher. It brings this month's rally to about four cents. If sustained, it would be the largest monthly advance since November 2022. It settled for the third consecutive session above its upper Bollinger Band, which is found slightly below $1.1170 today. It is consolidating quietly today in a roughly $1.1125-$1.1165 range. The US 2-year premium over Germany narrowed to about 155 bp yesterday. It has not been less than 150 bp since May 2023. The daily momentum indicators are moving higher, but overextended. Sterling has a five-day advance in tow and is trying to extend it to a sixth session today. In this run, it rallied more than three cents. In fact, sterling bottomed this month on August 8 near $1.2665. It has appreciated by a little more than 4.5 cents to almost $1.3130 today. Last year's high was set in mid-July around $1.3140. The 2022 high was about six cents higher. Sterling settled well above its upper Bollinger Band (~$1.3095 today). The momentum indicators are getting stretched, as one would imagine give the run-up.

America

The revisions to the US job growth means that rather than create 246k jobs a month in the year through April, it created only 178k. The reduction of aggregate hours worked means that productivity was greater and unit labor costs were lower than estimated. Less worked hours means that income was lower, but if consumption is not revised down, then savings will be. The futures market lifted the offs of a 50 bp cut next month to 40%. It was almost 35% at Tuesday's close and near 25% at Monday's settlement. Meanwhile, the market priced in nearly 105 bp of cuts this year, up from 99 bp Tuesday and a little more than 93 bp on Monday. This is a busy day for US data ahead of Fed Chair Powell's speech at Jackson Hole tomorrow. Weekly jobless claims have fallen in the past two weeks but likely edged up in the week ending August 16. Note that as of the previous week, the four-week moving average was 236.5k, slightly lower than the four-week moving average in the same week a year ago (244k). The US manufacturing PMI slipped below 50 in July for the first time this year, and likely holding below it now. Regional Fed surveys warn of possible weakness in the service PMI, which stood at 55.0 in July, the highest since April 2022. The composite eased to a three-month low in July (54.3) and is expected to have softened for the second consecutive month. Lastly, existing home sales may have risen for the first time in five months. For its part, Mexico offers a revised estimate of Q2 GDP (0.2% quarter-over-quarter and 2.2% year-over-year). More importantly, it will provide an estimate of inflation for the first half of August. The median forecast in Bloomberg's survey has the headline rate easing to 5.31% (from 5.52%), while the core rate is expected be at 4.07% (from 4.08%). Tomorrow, Canada reports June retail sales. They are seen falling by about 0.3%. They have fallen every month this year but April. Meanwhile, Canada's two largest railways (~80% of the national rail system) have been idled by a lockout after management and union talks floundered. The dispute centers around scheduling. Some cargo had reportedly already been diverted to the US. In the US, a dock worker strike looms. There has been a surge of US imports and inventory build that link to preparation for both labor disputes.

The rail strike in Canada has not prevented continued gains in the Canadian dollar. The US dollar extended its slide against the Canadian dollar and settled yesterday below the 200-day moving average for the first time in five months. It took some time, but the greenback broke CAD1.3600 on a settlement basis, which it had not done since early April. The high for the year was set on August 5 near CAD1.3945. It has approached CAD1.3570 today. The next support area is near CAD1.3550. The US dollar jumped by more than 1.5% against the Mexican peso for the second consecutive day. Recall that before this week the greenback had fallen in seven of the previous eight sessions. This week, it has almost completely recouped its losses, returning to the MXN19.4050. It is trading quietly so far today, pinned in the upper end of yesterday's range. Above there, the next chart area is near MXN19.60. The peso's loss was the largest in the world yesterday. Among emerging market currencies, the Colombian peso was a distant second, falling slightly less than 0.5%. The Chilean peso led the emerging market complex with nearly a 1% gain, aided perhaps by copper's highest close in a month.

REGISTRATION LINK

https://one.exnesstrack.net/boarding/sign-up/a/uq2cbl5o/?campaign=24533