USD extends losses, Yen gains

The week starts on a mixed note in Asia, after major US indices recorded their best week since last October and boosted appetite in global risk markets. A softer-than-expected CPI read in the US combined with robust retail sales and weekly jobless claims data boosted the expectation that the Fed could eventually achieve a soft landing. Goldman Sachs cut its recession forecast from 25% to 20%. The return of the carry positions in the yen last week also helped boosting appetite in the riskier pockets of the market. As a result, the S&P500 rallied almost 4% last week and is up by more than 8% since the dip we saw at the beginning of the month, Nasdaq 100 rallied more than 5% last week and is up by almost 12% since the August dip, the Dow Jones gained almost 3% last week and 6% since the August dip and the Russell 2000 recovered nearly 3% as well last week and has rebounded by more than 7% since its dip earlier this month. The Stoxx 600 recovered more than 6% since the August dip and the Japanese Nikkei soared almost 22%. In summary, it looks like the mini panic of the beginning of the month has well reversed. The VIX index is back to the pre-panic levels.

What’s next?

The US dollar starts the week downbeat. We don’t have a busy economic calendar this week, but the central bank policies and rate discussions will be on the menu of the week as the annual Jackson Hole meeting will begin on Thursday, Federal Reserve (Fed) Chair Jerome Powell will speak on Friday, and many other central bankers will speak at the event. Although Jackson Hole witnessed important policy pivots in the past and is a place where important twists and tweaks could happen, there is little potential for further dovishness regarding the Fed policy when Powell speaks later this week. There is nothing out there – at least in the data that’s available to us – that suggests that the Fed should announce a jumbo rate cut at the September meeting. We will be looking for a hint of what will happen after the September rate cut.

Price-wise, the US dollar is softer on Monday, the dollar index is testing the August support at the time of writing. The market pricing remains more dovish than what the Fed is set to deliver at the September meeting (with around 30% probability given to a 50bp cut), and also more dovish than what the Fed could deliver for the rest of the year. Therefore a USD rebound is plausible. The EURUSD which pushes higher above the 1.10 level and Cable that is preparing to re-test the 1.30 should have a limited upside potential.

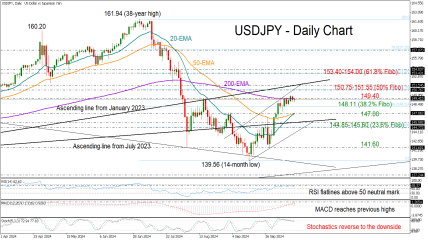

The Japanese yen, on the other hand, is better bid this morning. The USDJPY fell to 146 after the failure to clear the 150 offers last week. The Bank of Japan (BoJ) Governor Ueda will attend a special session in the Japanese parliament this week and will keep an accommodative tone. But the net speculative yen positions turned positive for the first time since March 2021 and big players are increasing bets that the BoJ will continue hiking the rates despite the sharp market reaction. The 150 level could act as a decent resistance to the USDJPY and keep the yen upbeat despite a cautious BoJ.

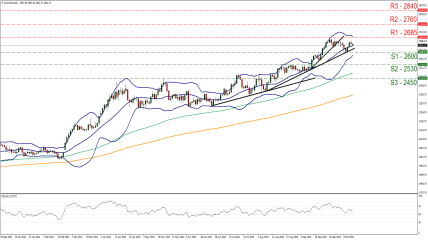

Elsewhere, the Fed rate cut bets sent gold to a fresh record last week, the yellow metal traded at $2500 per ounce, while oil hardly got a sentiment boost from improved market mood. The non-escalation of tensions in the Middle East and the sluggish Chinese data keep oil in the hands of the bears. US crude is trading near $76pb this morning, while Brent crude kicks off the week below $80pb mark.